6. Decomposing time series¶

Decomposing time series consists in extracting several time series from a

time series. These extracted time series can represent different components,

such as the trend, the seasonality or noise. These kinds of algorithms can be

found in the pyts.decomposition module.

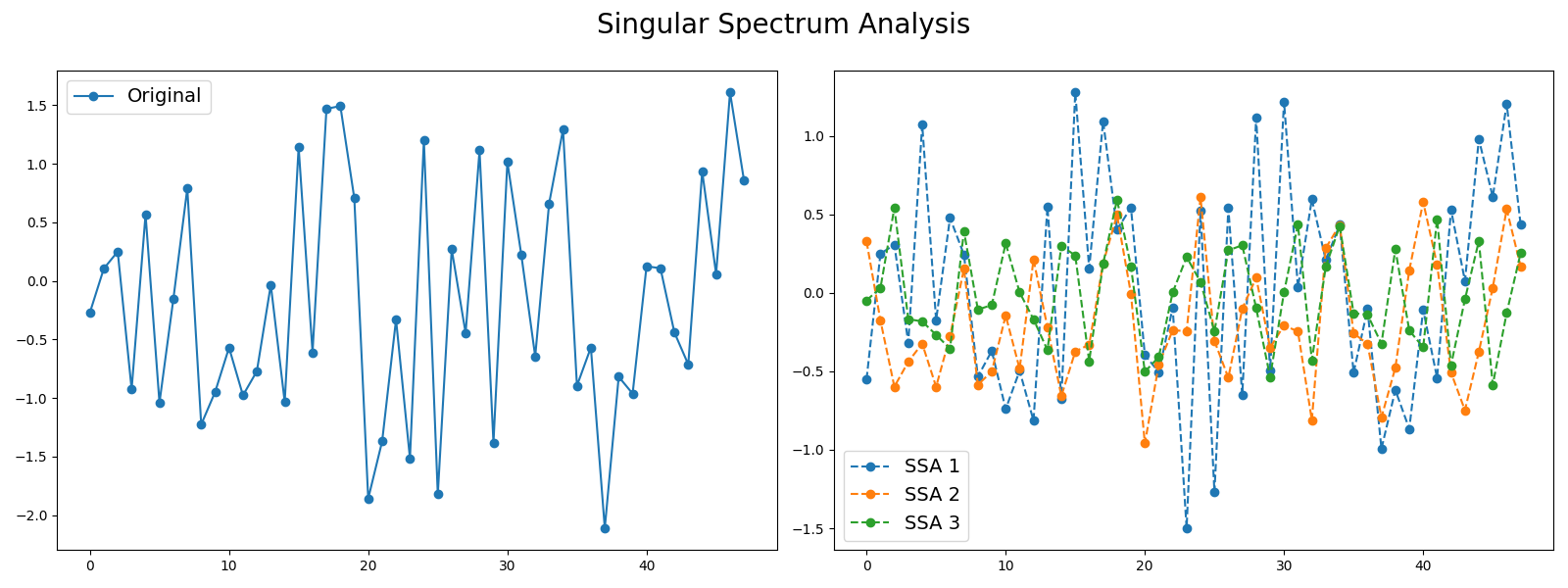

6.1. Singular Spectrum Analysis¶

SingularSpectrumAnalysis is an algorithm that decomposes a time

series  of length

of length  into several time series

into several time series  of

length such that

of

length such that  . The smaller the index

. The smaller the index

, the more information about it contains. The higher the index

, the more noise it contains. Taking the first extracted time series

can be used as a preprocessing step to remove noise.

, the more information about it contains. The higher the index

, the more noise it contains. Taking the first extracted time series

can be used as a preprocessing step to remove noise.

>>> from pyts.datasets import load_gunpoint

>>> from pyts.decomposition import SingularSpectrumAnalysis

>>> X, _, _, _ = load_gunpoint(return_X_y=True)

>>> transformer = SingularSpectrumAnalysis(window_size=5)

>>> X_new = transformer.transform(X)

>>> X_new.shape

(50, 5, 150)

References

- N. Golyandina, and A. Zhigljavsky, “Singular Spectrum Analysis for Time Series”. Springer-Verlag Berlin Heidelberg (2013).