Note

Click here to download the full example code

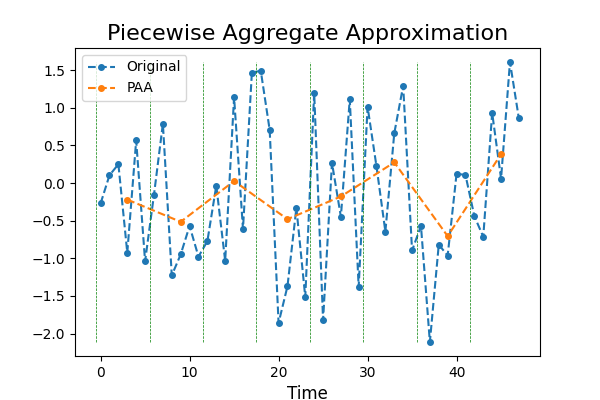

Piecewise Aggregate Approximation¶

Time series with a high sampling rate can be very noisy. In order to reduce

noise, a technique called Piecewise Aggregate Approximation was invented,

consisting in taking the mean over back-to-back points. This decreases the

number of points and reduces noise while preserving the trend of the time

series. This example illustrates the transformation.

It is implemented as

pyts.approximation.PiecewiseAggregateApproximation.

# Author: Johann Faouzi <johann.faouzi@gmail.com>

# License: BSD-3-Clause

import numpy as np

import matplotlib.pyplot as plt

from pyts.approximation import PiecewiseAggregateApproximation

# Parameters

n_samples, n_timestamps = 100, 48

# Toy dataset

rng = np.random.RandomState(41)

X = rng.randn(n_samples, n_timestamps)

# PAA transformation

window_size = 6

paa = PiecewiseAggregateApproximation(window_size=window_size)

X_paa = paa.transform(X)

# Show the results for the first time series

plt.figure(figsize=(6, 4))

plt.plot(X[0], 'o--', ms=4, label='Original')

plt.plot(np.arange(window_size // 2,

n_timestamps + window_size // 2,

window_size), X_paa[0], 'o--', ms=4, label='PAA')

plt.vlines(np.arange(0, n_timestamps, window_size) - 0.5,

X[0].min(), X[0].max(), color='g', linestyles='--', linewidth=0.5)

plt.legend(loc='best', fontsize=10)

plt.xlabel('Time', fontsize=12)

plt.title('Piecewise Aggregate Approximation', fontsize=16)

plt.show()

Total running time of the script: ( 0 minutes 0.223 seconds)